Understanding Startup Investment Stages: A Practical Guide for Angel Investors

If you are active in angel investing or considering getting more involved, you have likely encountered terms like pre-seed, seed, and Series A. These labels are widely used, often loosely defined, and occasionally misunderstood. Still, they provide a useful framework for understanding how startups evolve, how risk changes over time, and where you as an investor can play a role.

This overview walks through the startup lifecycle from the earliest capital to later-stage growth, with a particular focus on pre-seed and seed, where most angel investors operate.

Why Stages Matter

Startup stages are not arbitrary. They signal three things:

How much the business has been validated

What the company needs capital for

The type of risk you are taking as an investor

Earlier stages are driven by uncertainty and potential. Later stages are driven by execution and scaling. Understanding this progression allows you to align your investment strategy with your risk tolerance and expected return profile.

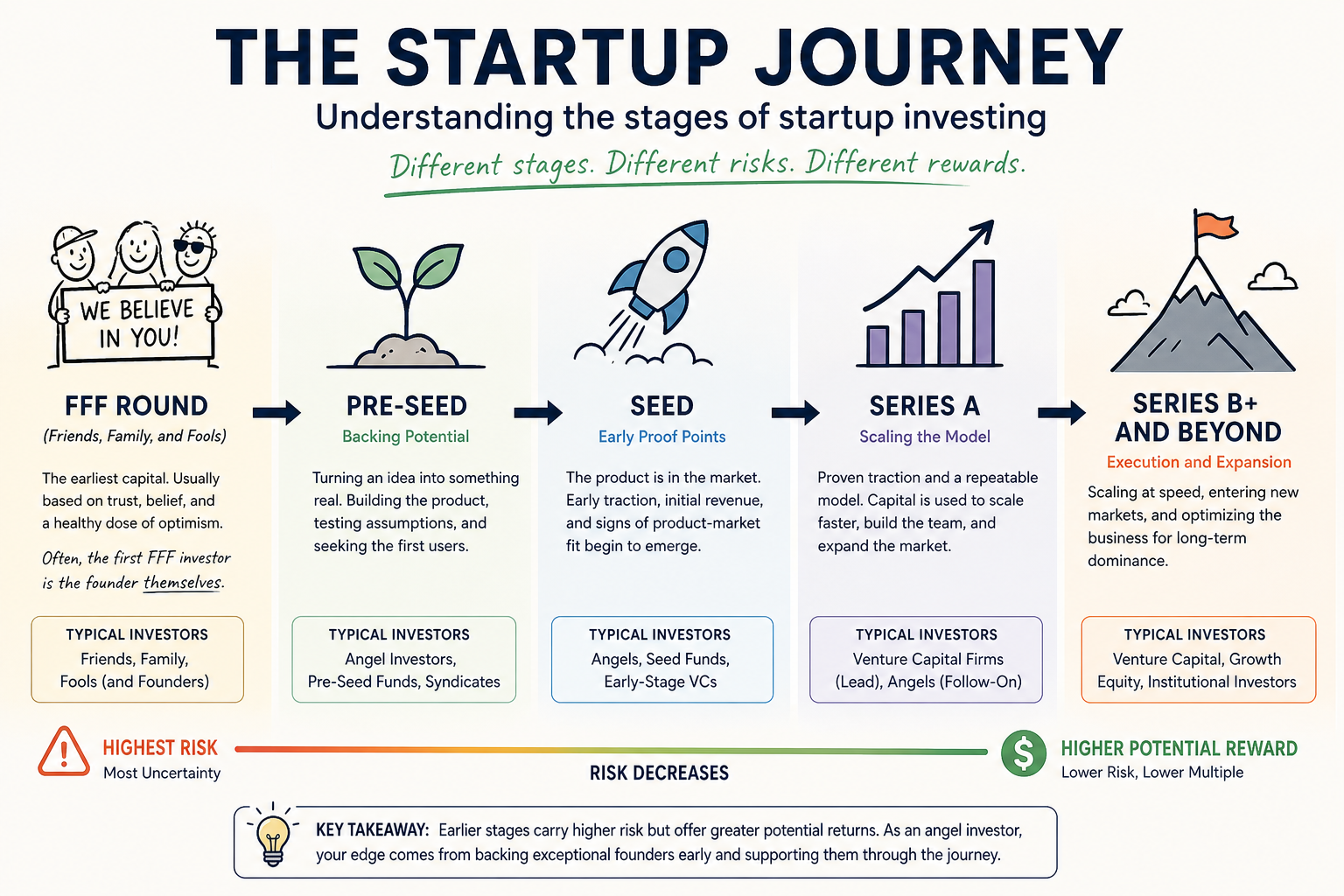

The FFF Round: Friends, Family, and Fools

Before pre-seed, there is an informal stage often referred to as the “FFF round” which stands for Friends, Family, and Fools.

The name is not entirely charitable, but it reflects a simple reality: at this stage, people are investing based almost entirely on trust in the founder rather than any meaningful business validation.

Typical characteristics include:

An idea, often still evolving

No product or an extremely early prototype

No revenue

A founder trying to get something off the ground with limited resources

In many cases, the first “FFF investor” is the founder themselves. Personal savings, credit cards, and opportunity cost are usually the initial capital sources. External FFF investors often include close personal relationships who are willing to take a leap based on belief rather than data.

From a formal angel investing perspective, this stage is often out of scope. However, it is important context because by the time you see a deal, the founder has typically already taken this initial risk.

The key takeaway is simple: if the founder is not meaningfully invested financially or otherwise at this stage, that is a signal worth paying attention to.

Pre-Seed: Backing Potential

Pre-seed is where structured early-stage investing begins. The company has moved beyond pure concept, but it is still very early.

Typical characteristics include:

A defined problem and initial solution approach

A prototype, MVP, or early product build

Minimal or no revenue

A small founding team, often still being formed

Capital at this stage is used to:

Build and iterate on the product

Test demand in the market

Reach initial users or customers

Investments are typically made by angel investors, small syndicates, and pre-seed funds.

At pre-seed, you are primarily underwriting the founders. There is limited data, so the evaluation centers on:

Founder quality and execution ability

Understanding of the problem

Speed of iteration

This is where the highest upside exists, but also where failure rates are highest. Most companies at this stage will not reach a successful exit, and many will not progress to the next round.

Seed: Early Proof Points

Seed-stage companies have begun to show evidence that the idea has merit.

Typical characteristics include:

A product in the market

Early users or paying customers

Initial traction, either in revenue or usage

Early signs of product-market fit

Capital raised at this stage is typically used to:

Refine the product

Build customer acquisition channels

Expand the team

Improve retention and engagement

Rounds are larger than pre-seed and often include a mix of angels, seed funds, and early-stage venture capital firms.

For angel investors, this is where evaluation becomes more data-informed. You are still assessing the founders, but you now have early metrics to analyze:

Are customers sticking around?

Is usage growing?

Is revenue trending in the right direction?

The key question shifts from “Can this work?” to “Is this starting to work in a scalable way?”

Risk remains significant, but it is no longer purely speculative.

Series A: Scaling the Model

At Series A, the company is expected to have established some level of product-market fit and is preparing to scale.

Typical characteristics include:

Consistent growth in revenue or user base

A clearly defined customer segment

Early repeatability in sales or acquisition

A more developed team

Capital is used to accelerate growth, build infrastructure, and strengthen operations.

Series A rounds are typically led by venture capital firms, with larger check sizes and more structured terms.

For most angel investors, participation at this stage is either through follow-on investments in earlier deals or via syndicates.

Series B and Beyond: Execution and Expansion

Later-stage rounds focus on scaling a proven model.

Typical characteristics include:

Meaningful revenue, often in the millions

Established market presence

Defined growth strategy

Operational maturity

Capital is used to expand geographically, increase market share, and optimize performance.

At this stage, investors are primarily underwriting execution risk rather than concept risk. Returns tend to be more predictable, but the upside multiple is typically lower than early-stage investments.

Where Angel Investors Add Value

In practice, most angel investors operate at the pre-seed and seed stages.

This is where:

Check sizes align with individual investors

Access is driven by networks and relationships

Founders benefit from hands-on support

Early-stage investing is not just about capital. It is about judgment, pattern recognition, and the ability to support founders when outcomes are still uncertain.

It also requires a realistic mindset:

Many investments will not return capital

A small number will drive the majority of returns

Time horizons are long

Diversification is not optional in this asset class. It is fundamental.

A Practical Perspective

While stages are useful, they are not precise. A seed-stage company in one ecosystem may look like a pre-seed company in another. Market conditions, geography, and sector all influence how these stages are defined.

As an investor, your goal is not to label a company perfectly. It is to understand:

How much risk is present

What has been validated

What still needs to be proven

Stages are simply a shorthand for those factors.

Final Thoughts

For angel investors, the most relevant opportunities typically occur before institutional capital fully takes over. That means getting comfortable with ambiguity, making decisions with incomplete information, and backing people as much as ideas.

The FFF stage sets the foundation. Pre-seed tests the initial hypothesis. Seed begins to validate it. Everything beyond that is about scaling.

Understanding this progression will help you make more informed decisions and build a more intentional portfolio over time.

In future posts, we will go deeper into how to evaluate founders, assess early traction, and structure your investments.